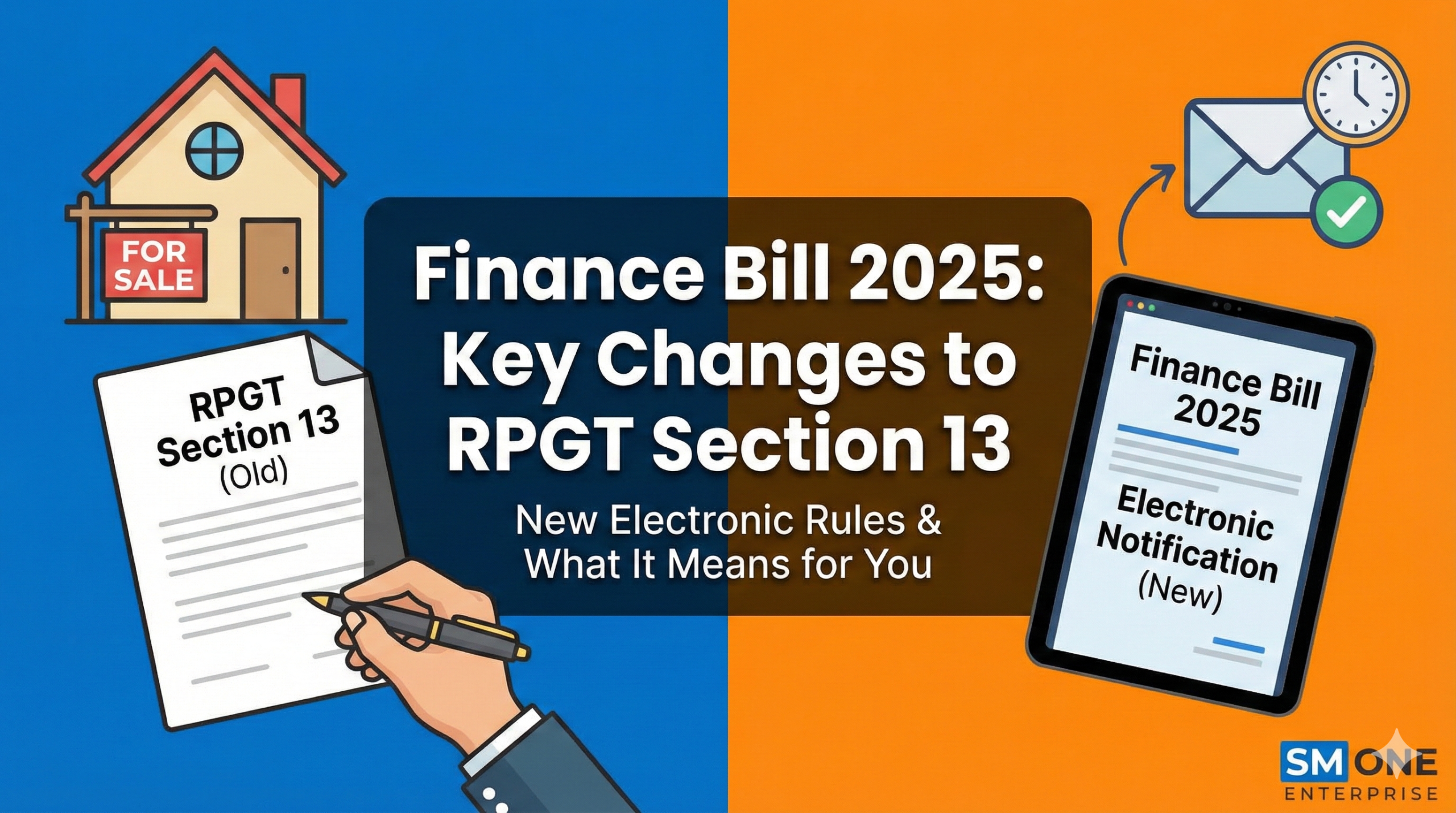

If you have ever been involved in a property transaction in Malaysia, you know that filing Real Property Gains Tax (RPGT) returns can be a race against time. Under Section 13 of the RPGT Act, both the disposer (seller) and the acquirer (buyer) are required to file returns within 60 days of the disposal.

However, the Finance Bill 2025 is set to change how these returns—and the critical notification of tax payable—are handled.

The bill introduces two new subsections—Section 13(8) and Section 13(9)—which push RPGT compliance into the digital age. This isn’t just a minor administrative update; it fundamentally changes the legal timeline for when a buyer is considered “notified” of their tax withholding duties.

Here is a complete guide to understanding these changes and how they affect property transactions starting in 2025.

1. The New Requirement: Section 13(8)

Streamlining Communication Between Seller and Buyer

Previously, notifying a buyer about how much tax to withhold was often a manual process involving separate letters or calculations.

Under the new Section 13(8), a disposer who files their RPGT return electronically may now automatically notify the acquirer of the tax payable based on that return.

Why this is important: Under Section 21B, the acquirer is required to retain part of the purchase consideration to cover the seller’s RPGT liability.

-

Old Way: The seller manually informs the buyer, risking delays or miscommunication.

-

New Way: The seller notifies the acquirer using the same figures submitted to the Inland Revenue Board (IRB).

This change clarifies the exact amount the buyer needs to withhold, speeding up the entire process.

2. The “Deemed Served” Rule: Section 13(9)

Electronic Service of Notification

This is the most critical change for buyers to be aware of. Section 13(9) introduces a strict rule regarding when the notification is considered received.

The notification under Section 13(8) is deemed served on the acquirer on the same day it is furnished electronically to the DGIR.

What this means for you: Once the seller hits “submit” on their electronic notification to the IRB, the law treats the buyer as having received it instantly.

This eliminates common disputes such as:

-

❌ “I never received your letter.”

-

❌ “You emailed the wrong address.”

-

❌ “Postal delays affected the withholding timeline.”

Real-Life Scenario: How It Works

To make this clearer, let’s look at a practical example involving a seller, Mr. Ali, and a buyer, Ms. Lim.

The Scenario:

-

Disposal Date: 1 March 2026

-

Transaction: Mr. Ali sells a shop lot to Ms. Lim for RM1,000,000.

-

Obligation: Mr. Ali must file his return within 60 days.

Step 1: Mr. Ali Files Electronically On 20 March 2026, Mr. Ali files his RPGT return electronically. He declares a disposal gain of RM200,000 and calculates the RPGT payable as RM20,000.

Step 2: Electronic Notification (Section 13(8)) At the same moment he files his return, he submits the notification of tax payable electronically to the IRB.

Step 3: The “Deemed Served” Effect (Section 13(9)) Even if Ms. Lim has not personally opened her email or checked her portal yet, the law automatically deems that she has been served with the notification on 20 March 2026—the exact same day Mr. Ali submitted it.

Step 4: Ms. Lim’s Obligation Because she is legally deemed notified, Ms. Lim must now:

-

Retain the required money from the purchase price.

-

Remit it to the IRB within the stipulated 60-day period (based on Section 21B requirements).

Why This Amendment Matters

This shift towards digitalization brings three major benefits to the Malaysian property market:

-

It Improves Efficiency: Electronic service removes the “he said, she said” disputes about whether a notice was received.

-

It Aligns with Digitalisation: Just like the recent e-Invoice implementation, RPGT processes are modernizing to ensure faster, transparent data flow.

-

It Provides Legal Certainty: Acquirers now have a clearly defined start date for their withholding obligations, reducing the risk of accidental non-compliance.

-

It Strengthens Enforcement: Acquirers can no longer claim they “did not know” about the tax payable to avoid their withholding duties.

SMONE: Your Partner in Tax Compliance

Navigating legislative changes like the Finance Bill 2025 can be complex for both individuals and businesses. Whether you are a property investor needing to file RPGT or a company managing tax withholdings, accuracy is key to avoiding penalties.

SMONE’s Tax & Compliance Services ensure that your statutory obligations are met on time, every time. We handle the calculations and submissions so you can focus on your investments.

Need help understanding your RPGT obligations? Contact us today to speak with our consultants.