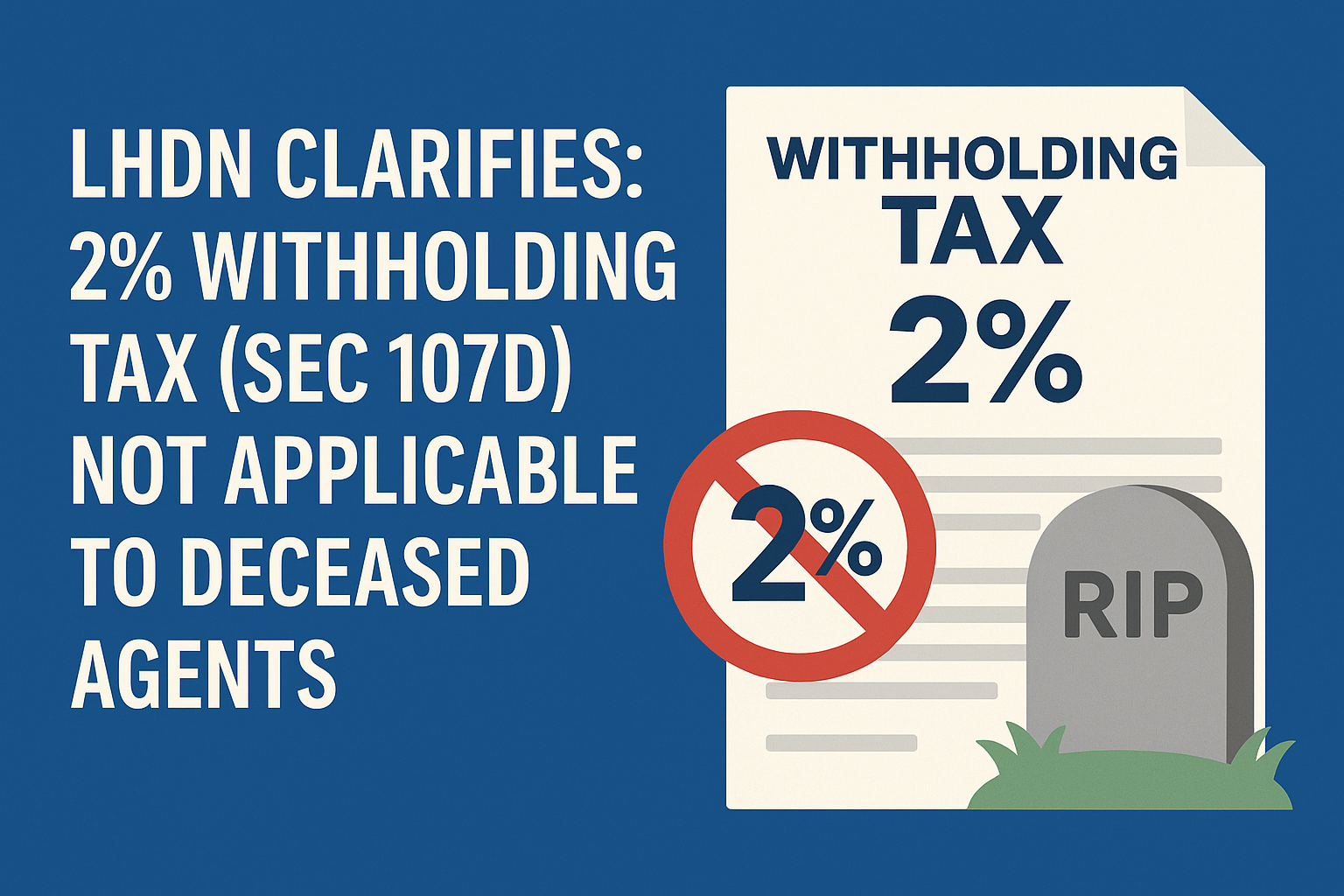

The Inland Revenue Board of Malaysia (LHDN or HASiL) has issued a significant press release today, June 30, 2025, to clarify the application of the 2% withholding tax under Section 107D of the Income Tax Act 1967. The clarification specifically addresses the situation involving payments made to agents, dealers, or distributors (referred to as EPP) who have passed away.

This official statement provides much-needed clarity for companies that make commission-style payments and for the families and executors of deceased individuals.

A Quick Recap: What is Section 107D?

As a brief background, Section 107D of the Income Tax Act 1967 requires companies to deduct a

2% withholding tax on any cash payments made to their resident individual agents, dealers, and distributors. This tax is then remitted to LHDN. The purpose of this rule is to improve tax compliance among this group of earners.

LHDN’s Key Clarification: Tax Withholding Ceases After Death

The central point of the new announcement is a clarification based on the legal definition of an “individual”.

-

The Ruling: Under the Income Tax Act, an “individu” is defined as a living natural person. LHDN has clarified that once an agent, dealer, or distributor (EPP) passes away, they are no longer categorized as an “individu” under the act.

-

The Consequence: Therefore, the 2% tax deduction under Section 107D is no longer applicable to any payments made to the deceased EPP.

- Effective Date: LHDN will no longer accept these 2% tax deduction payments for deceased individuals starting from August 1, 2025.

So, What Happens to Income Received After Death?

This does not mean the income becomes tax-free. Instead, the responsibility for managing the tax on this income shifts from the paying company to the deceased person’s estate.

- Responsibility of the Estate: Any income received after the date of death must be managed by the deceased’s legal representative, such as the executor (

wasi), administrator (pentadbir), or heir. - New Tax File Required: This representative is required to report this income by registering a Deceased Person’s Estate Tax File (Fail Cukai Harta Pusaka – TP) with LHDN.

- How to Register: To do this, the representative must complete the Taxpayer Registration Notification Form (CP57) and submit it to any LHDN office along with the following documents:

- A copy of the death certificate.

- A copy of the grant of probate or letter of administration.

Action Plan for All Parties

LHDN advises all parties to take note of this ruling and act accordingly.

For Paying Companies:

- Cease Withholding: From August 1, 2025, stop withholding the 2% tax for any payments made in the name of a deceased agent.

- Verify Payee: Ensure all future payments are made to the proper legal representative of the deceased’s estate.

For Heirs / Executors of a Deceased Agent’s Estate:

- Register the Estate Tax File: Promptly register a new tax file (TP) for the estate to manage all income received after the date of death.

- Report All Income: Ensure all income received by the estate is properly reported under this new tax file.

Navigating Complex Tax Situations with SMONE

Managing the tax affairs of a deceased individual’s estate can be a complex and emotional process, requiring careful adherence to specific legal and tax procedures.

At SMONE, we understand the sensitivity and complexity of these situations. We can provide expert advisory and support to both companies and estate representatives to ensure these matters are handled correctly. We work with our network of tax and legal professionals to guide you through the process, from registering the tax file to ensuring all compliance matters are settled smoothly.

Contact us today for a professional and confidential consultation.

(Disclaimer)

This article is for general informational purposes and is based on the LHDN media statement dated June 30, 2025. It does not constitute legal or tax advice. Please consult with a qualified professional for advice tailored to your specific situation.